Partnership Income Tax Malaysia

Resident companies are taxed at the rate of 24. Tax Treatment of LLP.

Tax Season Is Coming Malaysia Business Income Tax Deadlines For 2022

Individuals Two companies Individual and Company Individual and trustee RESPONSIBILTIES To get and complete a copy of Income Tax Return Form P from the nearest LHNDM Branch if the form does not reach on time To prepare statement of.

. In the boxes provided. The companies must not be part of a group of companies where any of their related companies have a paid-up capital of more than RM25. D 0012345602 D 3 Reference no.

Resident company with a paid-up capital of RM 25 million or less and gross income from business of not more than RM 50 million. Although a partnership is not subjected to pay tax it still has to file an annual income tax return to show all income earned and business expenses deducted by the partnership during the year. INTRODUCTION Gains or profits from carrying on a partnership are liable to tax.

For income tax purposes a partnership is not a chargeable person. Whereas in partnership the chargeable income is divided among the partners as an individual. Type of company.

Characteristics of a Partnership Characteristics of a partnership are based on its interpretation in accordance with the. Each of the partners will have a responsibility on the profit and loss based on their profit sharing ratio. Banjaran Pendapatan Cukai Pengiraan RM Kadar Cukai RM 0 - 5000 5000 pertama 0 0.

24 in excess of RM 600000. Services performed or rendered in Malaysia paid to a public entertainer. 2 Income tax no.

However LLP with capital contribution of RM25 million or less will enjoy a preferential tax rate of 19 on the first RM 500000 of its chargeable income. Registration no Registration number with the Companies Commission of Malaysia. Partnership income tax no.

Individuals who earn an annual employment income of more than RM34000 and has a Monthly tax Deduction MTD is eligible to be taxed. In Malaysia the business profits of a partnership are not taxed at the partnership level but is taxed in the hands of each partner based on his share of income from the partnership at the relevant tax rate. It is not a separate legal entity which is.

Income tax rates. The SME company means company incorporated in Malaysia with a paid up capital of ordinary share of not more than RM25 million. Partnership will follow the tax rate of an individual.

In Malaysia partnership income is S 4 a business income. Rates of tax as per Part II Schedule1of ITA 1967. The current CIT rates are provided in the following table.

The calculation of individual threshold of non taxable income is taking into account after the deduction of annual gross income with eligible individual reliefs and tax rebates. Partnership can exist between. D 0012345602 5 Basis of Apportionment.

A Gains profit from a business. May 2016 Produced in conjunction with the. F Gains profit not falling under any of the foregoing paragraphs.

LLP have a similar tax treatment like Company where chargeable Income from LLP will be taxed at the LLP level at tax rate of 24 generally. 15 of gross amount. In the box provided.

4 Number of partners Enter the number of partners. 5 Basis of apportionment. Hence each partner is required to pay for their own income tax even though they are practising partnership.

17 on the first RM 600000. E Pensions annuities or other periodic payments. D Rent royalties or premiums.

For both resident and non-resident companies corporate income tax CIT is imposed on income accruing in or derived from Malaysia. Contents 1 Corporate Income Tax 1 2 Income Tax Treaties for the Avoidance of Double Taxation 5 3 Indirect Tax 7 4 Personal Taxation 8 5 Other Taxes 9 6 Free Trade Agreements 10. Partnership income tax no.

C Dividends interest or discounts. L Co Plt. LAW GOVERNING THE TAXATION OF THE PARTNERSHIP.

Resident companies are taxed at the rate of 24 while those with paid-up capital of RM25 million or less and gross business income of not more than RM50 million are taxed at the following scale rates. AF002133 201706002678 A member firm of Malaysian Institute of Accountants MIA Approved Company Auditor Income Tax Agent and GST Agent was established to assist Malaysia Small and Medium Enterprises on their company financial statement statutory audit taxation and SST Sales and Services Tax affairs. 41 Partnership A partnership is not a person in law.

The partnership could file Form P through paper-form submission or e-filling. D Enter the partnership income tax no. Income derived from the partnership is allocated to its partners based on the agreed profit sharing ratio and taxed in the hands of the partners.

B Gains profit from employment. Carried forward indefinitely to set off against future business income only unless. Corporate - Taxes on corporate income.

In the case of sole proprietorship business chargeable income is his or her individual income. D Enter the partnership income tax no. With paid-up capital of 25 million Malaysian ringgit MYR or less and gross income from business of not more than.

2 Income Tax No. Tax is imposed annually on individuals who receive income in respect of. For small and medium enterprise SME the first RM600000 Chargeable Income will be tax at 17 and the Chargeable Income above RM600000 will be tax at 24.

Resident company that does not control directly or indirectly another company that has paid-up capital of more than RM 25 million.

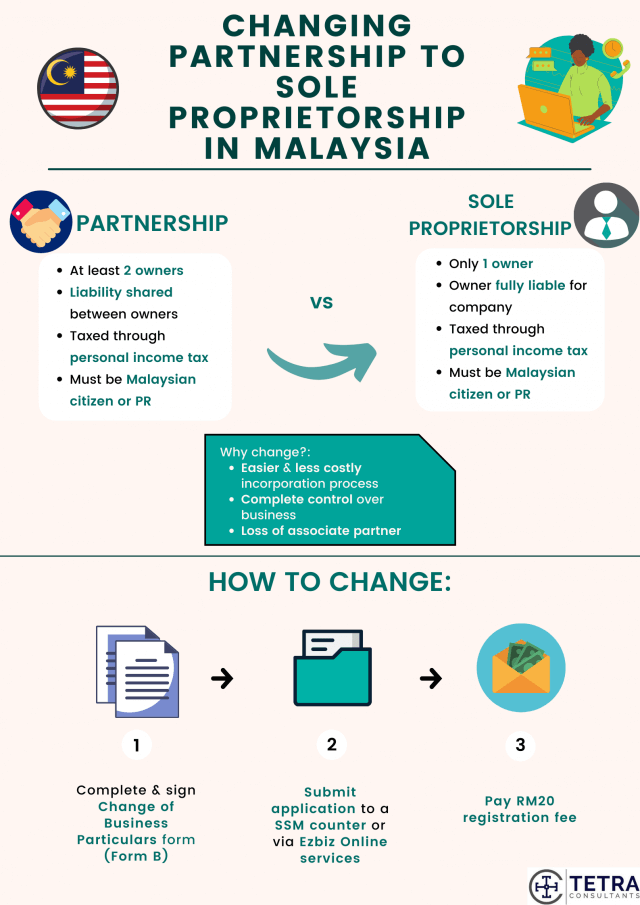

Steps To Change Partnership To Sole Proprietorship Company In Malaysia Tetra Consultants

7 Tips To File Malaysian Income Tax For Beginners

Business Income Tax Malaysia Deadlines For 2021

Deadline For Malaysia Income Tax Submission In 2022 For 2021 Calendar Year L Co

Income Tax Number Registration Steps L Co

2

0 Response to "Partnership Income Tax Malaysia"

Post a Comment